On 14 August 2001, ninety minutes after Jeff Skilling's surprise resignation crossed the wires, Sherron Watkins wrote to Rick Buy. Buy was Enron's Chief Risk Officer. Watkins had been at the company for two years. The email is short and sharp:

“I sure hope we make good use of the bad news about Skilling's resignation and do some house cleaning… I've been horribly uncomfortable about some of our accounting in the past few years and… I'm concerned some disgruntled employee will tattle. Can you influence some sanity?”

The reply from Buy is two and a half hours earlier in the thread — a placeholder from an unrelated exchange — but it captures the response anyway: “Take care, and lets have lunch in Sept.”

The Watkins memo most retrospectives quote is the anonymous one she sent to Ken Lay on 15 August — the next day. The Powers Report cites it. The PBS NewsHour profile cites it. The Senate Permanent Subcommittee on Investigations hearings cite it. The “tattle” line, the same-day-as-Skilling timing, the lunch-in-September brush-off from the company's own Chief Risk Officer — those don't appear to be part of the established public record.

We found that thread in twenty-three minutes, on a laptop, from a chat conversation. No subpoena, no archive request, no team of researchers. We pointed Clouseau at the public Cohen/CMU Enron Email Dataset — about 500,000 messages from 158 mailboxes, released in 2003 and picked over by journalists, prosecutors, and academics for two decades — and asked one question: Are there things in here that haven't already been written about?

What came back was the email above, plus three other documentary threads we hadn't seen in the standard secondary literature.

The method, brieflyHalf a million emails, one conversation.

A 181,338-email cut of the Cohen/CMU Enron release, read by Clouseau on a MacBook in about forty minutes. No cloud, no external service — the documents never leave the laptop. From asking the question to findings-with-citations: twenty-three minutes.

What follows is what came back. Where we can confidently say a finding doesn't appear in the standard public account, we say so. Where we can't fully rule out a buried trial-exhibit appearance, we say that too.

Finding 01The day-of warning to the Chief Risk Officer

The Watkins → Buy email above sits in Buy's inbox as buy-r/inbox/628.eml. The Powers Report names Buy as the Chief Risk Officer who failed to escalate concerns; it cites his role in general terms but doesn't quote a dated written warning from Watkins. The Globe and Mail, PBS NewsHour, the House Energy & Commerce hearing record, and the Senate PSI report all anchor to the Aug 15 anonymous memo to Lay. None surface the Aug 14 named email to Buy by date or content.

The phrase “disgruntled employee will tattle” is striking on its own — Watkins is signalling to the CRO that she may become that employee, framing whistleblowing as a managerial risk Buy should price in. Buy's recorded reply, regardless of which exchange in the chain it answers, was lunch in September. The Aug 22 face-to-face Watkins had with Lay is well-documented. The eight-day window before that meeting — during which the Chief Risk Officer received a dated written warning from a named senior accountant and deferred a substantive response — isn't.

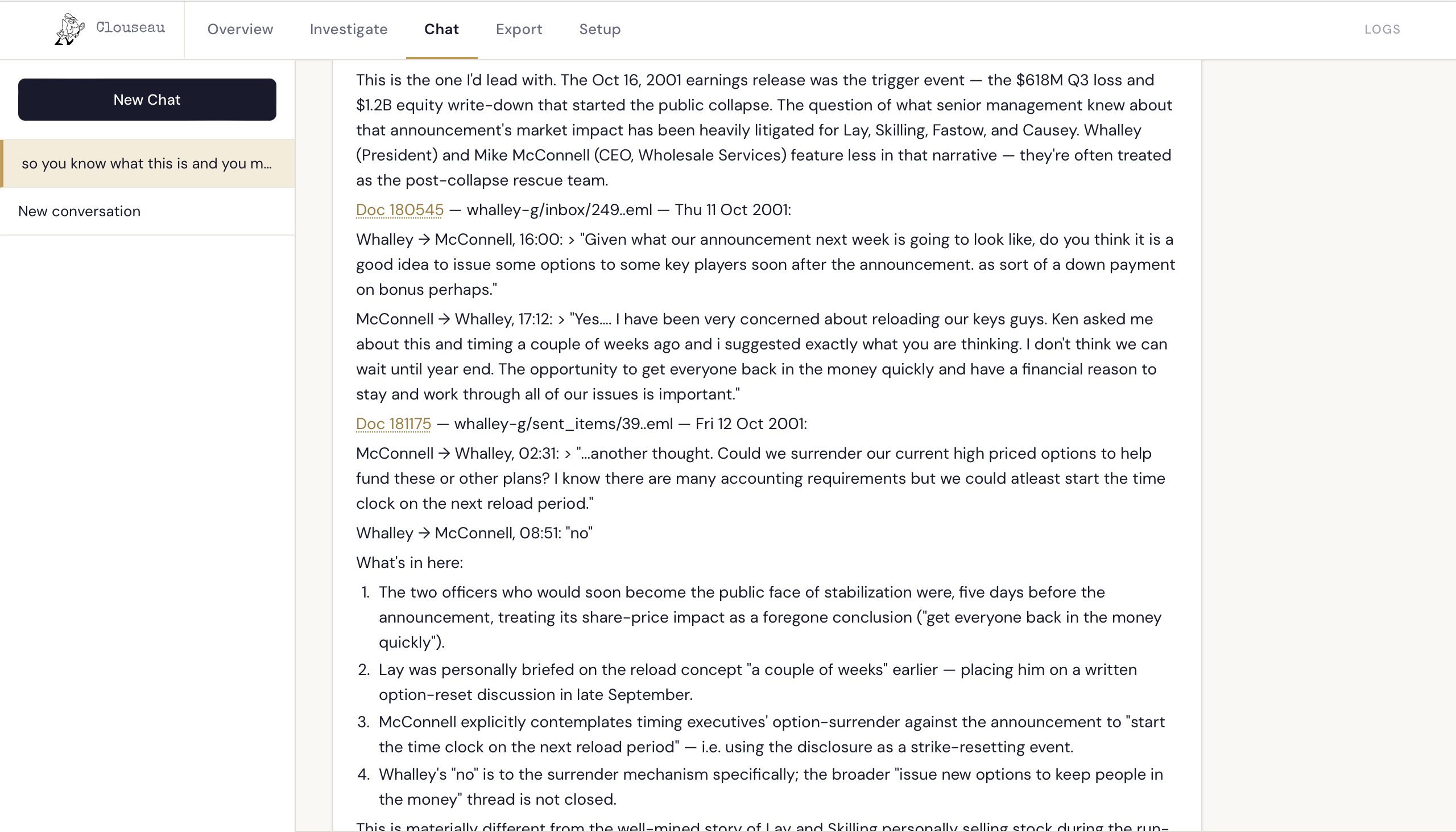

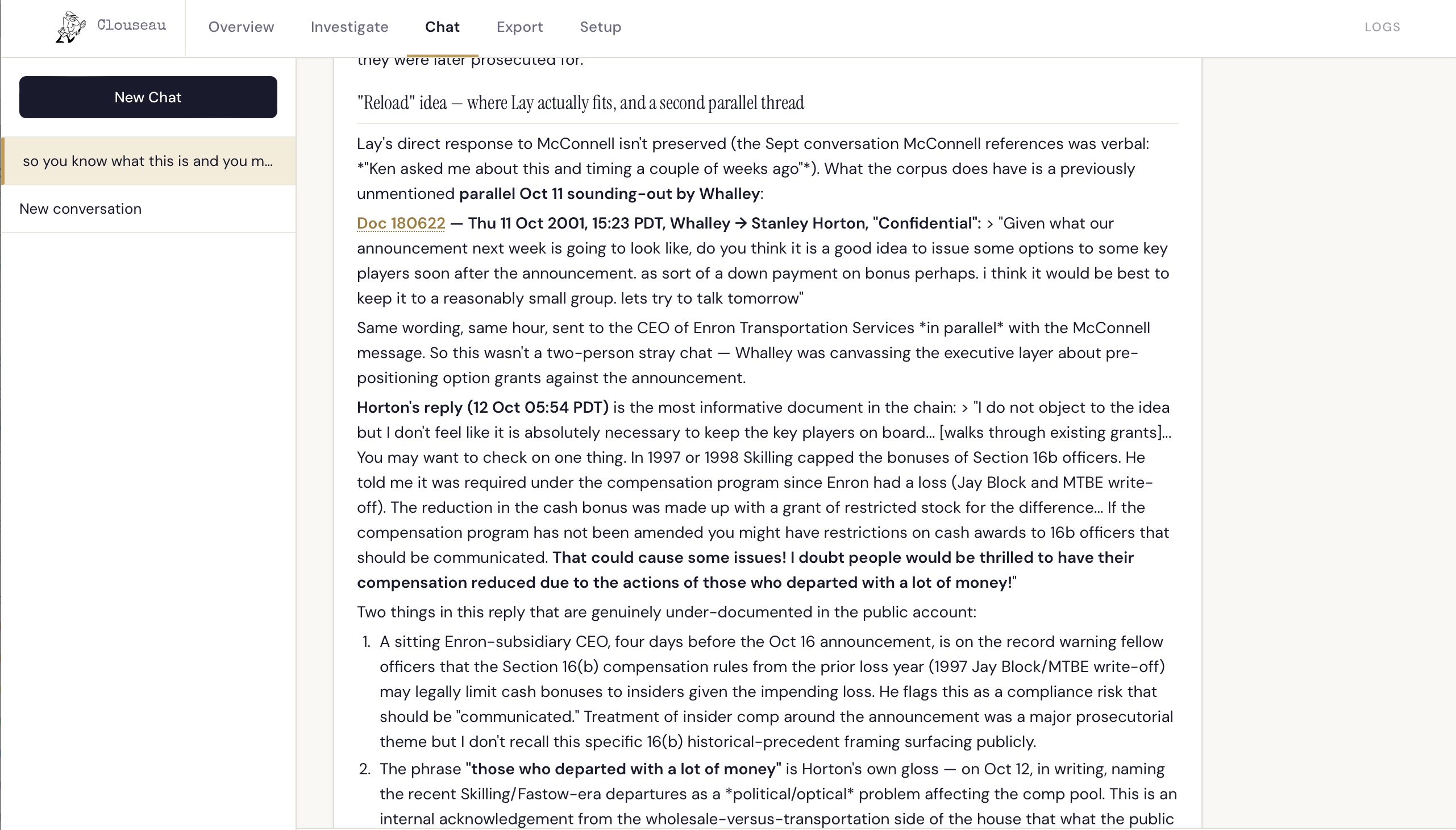

Finding 02Engineering executive options against a foreseeable price drop

Five days before the 16 October 2001 earnings announcement — the $618 million Q3 loss and $1.2 billion equity write-down that triggered the public collapse — Greg Whalley, then Enron's President, sent a four-line email to Mike McConnell, CEO of Wholesale Services:

Given what our announcement next week is going to look like, do you think it is a good idea to issue some options to some key players soon after the announcement. as sort of a down payment on bonus perhaps.

McConnell's reply is more revealing than the question:

Yes…. I have been very concerned about reloading our keys guys. Ken asked me about this and timing a couple of weeks ago and i suggested exactly what you are thinking. I don't think we can wait until year end. The opportunity to get everyone back in the money quickly and have a financial reason to stay and work through all of our issues is important.

Three details matter. “What our announcement next week is going to look like” treats the share-price hit as already known — five days before the market saw it. “Ken asked me about this… a couple of weeks ago” puts Ken Lay personally on the option-reset discussion. And get everyone back in the money quickly describes using the company's own price drop to reset strike prices.

The next morning, McConnell escalates the mechanic: “Could we surrender our current high priced options to help fund these or other plans?… we could atleast start the time clock on the next reload period.” Whalley's reply: “no” — to the surrender mechanism specifically. The broader thread, about pre-positioning option grants against the announcement, stays open.

This isn't a stray two-person discussion. The same day, Whalley sent the same message to Stanley Horton, CEO of Enron Transportation Services. Horton's reply, the next morning, is the most informative document in the chain:

I do not object to the idea but I don't feel like it is absolutely necessary to keep the key players on board…

You may want to check on one thing. In 1997 or 1998 Skilling capped the bonuses of Section 16b officers. He told me it was required under the compensation program since Enron had a loss… If the compensation program has not been amended you might have restrictions on cash awards to 16b officers that should be communicated. That could cause some issues!

I doubt people would be thrilled to have their compensation reduced due to the actions of those who departed with a lot of money!

Horton is a sitting Enron-subsidiary CEO, four days before the announcement, putting in writing two things: a Section 16(b) compliance flag against the impending loss-year cash bonuses, and the open acknowledgement that the recent Skilling/Fastow-era departures were already a political problem for the remaining officers' pay.

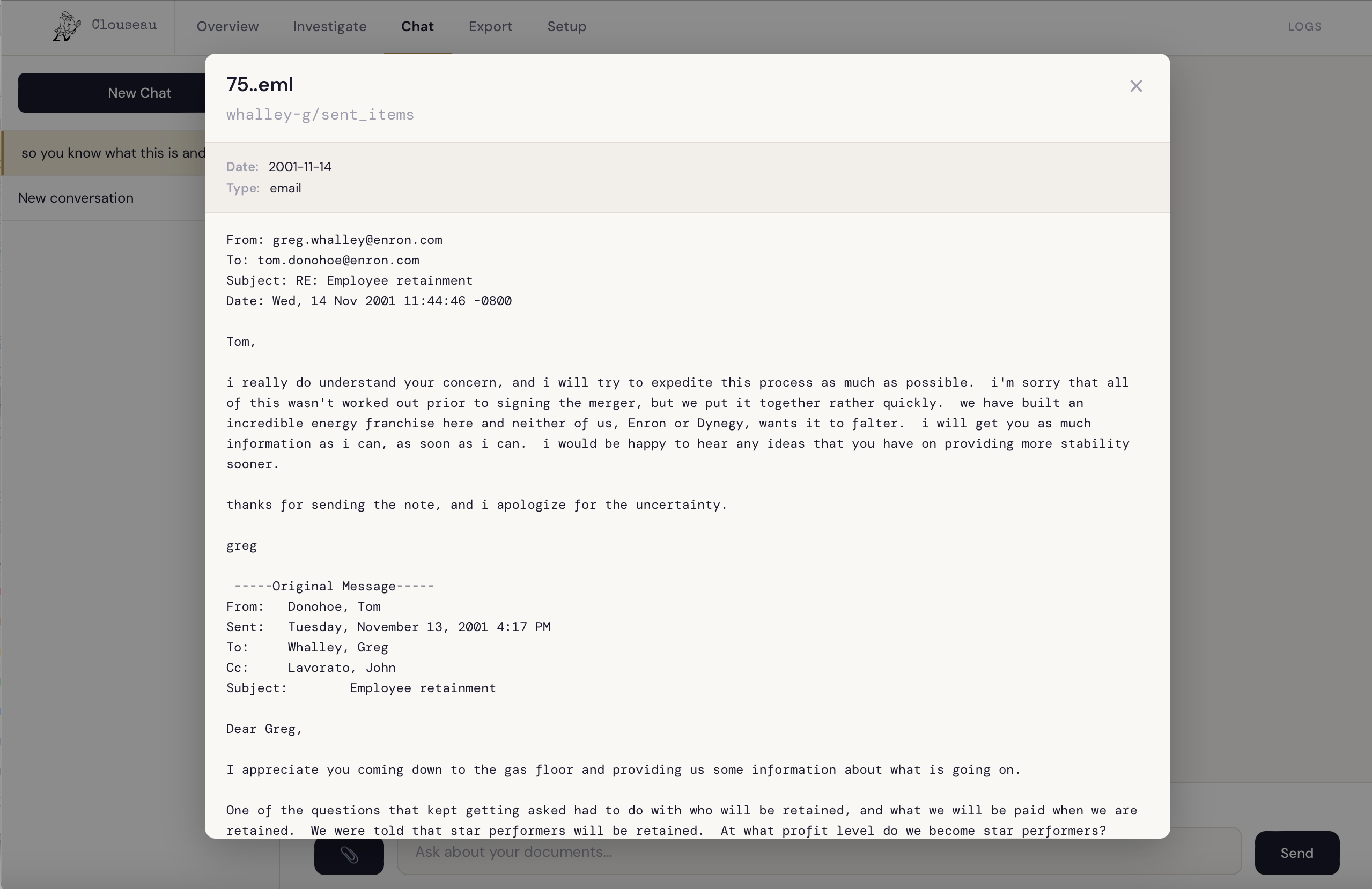

A month later, with Dynegy's rescue offer in motion, Tom Donohoe — a gas-floor trader — demanded retention clarity from Whalley and got back: “i'm sorry that all of this wasn't worked out prior to signing the merger, but we put it together rather quickly.” Five days before the announcement, the executives were canvassing each other about reload mechanics. A month later, the workforce was told retention hadn't been worked out.

The standard accounts — Powers Report, Senate PSI — turn on Fastow's LJM partnerships and board oversight, not this. Clouseau checked it against the live public record while it worked; none of those sources carry the October 11–12 sequence. It may sit in a trial exhibit somewhere. It isn't in the published histories.

Finding 03A director's WSJ answers, routed through the conflicted CFO

On 25 September 2001, Wall Street Journal reporter John Emshwiller sent five questions, by email, to Enron board member Dr John Mendelsohn — at MD Anderson Cancer Center, where Mendelsohn was president. The questions were specific, including:

1. Does he recall any questions coming before the board regarding the LJM2 Co-Investment, LP and the involvement of certain Enron officials in that partnership?

…

5. Is Dr. Mendelsohn familiar with the compensation level paid to the general partner of the LJM2 partnership?

Mendelsohn forwarded the questions through MD Anderson administrative staff to Karen Denne at Enron Investor Relations. Mark Palmer, Enron's PR head, wrote in the next email of the chain: “I forwarded them to Andy earlier today.”

Direct written questions to an independent board member, asking specifically about Fastow's LJM2 compensation, were filtered through Enron PR to Fastow personally before Mendelsohn answered them. PRWeek later covered the broader Lay/Palmer/Fastow tension around granting the WSJ interview. The specific mechanic — a sitting independent director's written board-oversight answers being routed through the conflicted CFO before reaching the reporter — is not in the public account.

Finding 04The LJM statement drafting list

Two days after the Mendelsohn routing, on 27 September 2001, Palmer circulated the draft WSJ LJM statement to a distribution list of seven: Lay, Whalley, Kean, Koenig, Derrick, Rieker — and Fastow himself. Fastow remained on Enron's messaging team for the public statement about his own related-party entity until 24 October, when he was placed on leave.

Koenig (Investor Relations) and Rieker (Investor Relations / Assistant Corporate Secretary) both later pled guilty to securities fraud connected to misleading investor disclosures from this period. Their presence on the drafting distribution list for the LJM statement places the messaging architecture squarely inside the documentary chain of conduct they were prosecuted for.

The PR-side Lay/Palmer/Fastow dispute around the WSJ coverage is in the public record. The specific Sept 27 distribution list — and the fact that the eventual cooperators were on it from the drafting stage — isn't a public talking point.

One thing worth flagging: the verification happened in the same conversation. Pulling the named threads out of half a million emails and checking each against today's public record — congress.gov, govinfo.gov, the contemporary press — wasn't a separate pass. It was the same twenty-three minutes.

What it showsThe same is true of your own documents

None of this overturns the Enron story. Skilling was convicted, Fastow served six years, the broad account won't change. But that account is a summary. It doesn't record which officer wrote what, on which day, to whom — the detail an investigation actually turns on. That detail sat in a public archive for twenty years because reading half a million emails by hand was never worth the time.

Your business holds the same kind of archive. A duplicate payment, a contract that lapsed out of compliance, a supplier nobody approved — if they exist, they are in your documents now, the same way these threads were in Enron's.

Clouseau reads them, and shows you the document behind every answer.

See it on your own documents.

Thirty minutes to see the app and talk through what you're looking for. If it fits, you can see what it finds on your own documents.

Book a demo